Real estate syndication deals have become quite popular especially among the doctor community.

Why?

It allows those too busy to deal with tenants to passively invest in real estate and still get the benefits such as tax advantages and cash flow distributions.

One of the questions new Passive Investment Circle members want answered is “how much do they get paid” over a period of time.

Seems like a logical question to me.

These investments use a “waterfall calculation” to structure and compensate the two main groups:

- General partner (GP, sponsors)

- Limited partner (LP, passive investors)

There are multiple ways in which waterfalls are designed and this article will help simplify how cash is distributed between the general partners and the limited partners via a distribution waterfall.

Don’t Miss Any Updates. Each week I’ll send you advice on how to reach financial independence with passive income from real estate.

Sign up for my newsletterWhat’s a Waterfall Distribution In Real Estate?

In order to best understand a waterfall structure, close your eyes and imagine what a waterfall looks like.

When water flows over a ledge into another body of water, it sometimes hits another ledge before flowing to the next level below it.

A real estate waterfall is similar to this.

It’s a legal term used in an Operating Agreement that describes how, when, and to whom funds are paid in real estate syndication deals.

It’s designed to ensure that the interests of GPs and LPs align in a way that properly compensates everyone involved in an investment.

As a passive investor, your distributions (passive income) will typically flow according to a waterfall distribution schedule. Think of this as a cascading structure of payments that flow in a specific order.

Waterfall Example

Here’s an example of what a basic waterfall structure looks like:

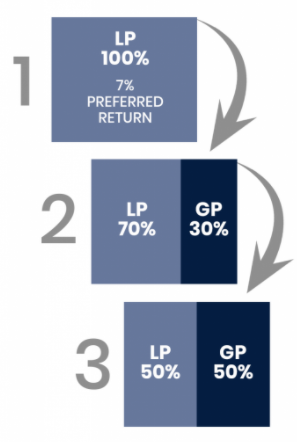

If you’re a limited partner in a deal with a 7% preferred return , this means you’re paid this amount before the general partners are paid. A preferred return or “pref” is typical of real estate deals and is the first cash distributions paid to equity partners.

After the pref takes place, then the cash flow splits can be done in a variety of ways between the LPs and GPs such as:

- 70/30

- 80/20

- 90/10

Waterfall structures occasionally rely on the internal rate of return (IRR) to trigger different payment scenarios.

For instance, when certain IRR hurdles are accomplished, a split between the GPs and LPs can change. This is set up to keep the GPs incentivized to do their job and get the best investment returns.

The preferred returns help the passive investors know that a certain return is guaranteed no matter the performance of the asset as they’re the primary equity capital source.

Because of this, they can rightfully expect to get their initial investment back along with a nominal amount of interest.

This ensures they receive adequate compensation for the risk they’ve taken as the majority capital provider in the deal.

How Is a Waterfall Return Structured?

One of the most important legal documents to review when investing in a syndication is the private placement memorandum (PPM).

Related article: Understanding Private Placement Memorandums For Syndications

Within the distribution section of the private placement memorandum, you’ll be able to see the common types of waterfall structures that’s been set up for the project.

This can include any of the following provisions:

#1. Preferred return “pref”

Remember that a preferred return refers to the ordering in which profits from commercial real estate projects are distributed to investors (LPs). It’s a threshold return that limited partners are offered prior to the general partners receiving payment. This can range anywhere from 5-9%.

#2. Equity splits

Once the pref has been made, there’s an equity split of the remaining returns between the GP and LP groups. As mentioned earlier, these can range from 50/50, 70/30, 80/20, etc. depending on how the waterfall structure is set up.

#3. Promote

The sponsor promote refers to the share of profit paid to the general partner “promoter” for a project. It’s also known as carry or carried interest in other forms of private equity investing.

#4. IRR hurdle

This is also known as XIRR or IRR lookback. In this model, a certain threshold or “hurdle” must be met to trigger new profit-sharing arrangements.

#5. Catch-up provision

This is similar to the IRR hurdle but requires that 100% of the returns go to the limited partners until a certain threshold is met. After that, any remaining funds go to the general partner.

#6. Simple split

Many of the syndications I’ve personally invested in have had a simple split structure. These are less complicated equity waterfall models that contains no IRR hurdles or prefs. All proceeds of the project are split between the LPs and GPs.

#7. Return of capital

Return of capital refers to the payments that the investors receive which returns a portion of the capital that they invested back to them. Usually provisions can be created to achieve a certain threshold of return of capital to an investor before the sponsor receives their returns.

#8. Capital event

A capital event is usually defined as one of two things – either the sale of the property, and/or a refinance of the property.

#9. Tiers

There are examples of two-tiered waterfall agreements that contain different rules for cash flow disbursements as well as capital events. So you may get a simple split for cash flow, whereas a capital event may contain different rules.

Why Are Distribution Waterfalls Important?

Distribution waterfall models outline all the rules for profit distribution in a real estate investment.

Most GPs like to keep things as simple as possible as to not confuse some of the newer limited partners that may not have much experience investing in syndications.

There’s many types of deal structures available and it’s a good idea to create your goals before you begin evaluating deals. For instance, there’s deals set up that allows LPs to get their initial investment back as soon as possible (refinance option) and there’s also those where the GP receives promote interests before the LPs receive their total investment.

In this case, it encourages better performance from the sponsors which leads to bigger profits.

Waterfall Calculations (Example #1)

Cash flow waterfall

Most deals I’m personally invested in have a 5-6 year hold period. A cash flow waterfall tells me how excess cash from a project will be distributed during this period.

Here’s a break down of the hurdle rates that are commonly used in this type of waterfall.

Bucket #1: Preferred Return Hurdle

It’s not uncommon to see 100% of the cash flow distributed to passive investors up to a certain amount (preferred return).

In this example, once the 7% pref is hit, then the cash flows will begin filling up the next bucket.

Bucket #2: Common Equity Hurdle

The excess cash inflows is now split 70/30 where 70% goes to the LPs and 30% to the operator. Once this bucket is filled up, the remaining cash will begin filling up the next bucket.

Bucket #3: Performance Hurdle

Bucket #3 is considered a performance-based hurdle based on the originally projected returns. For example, if the project had a 13% IRR projection then this hurdle would not come into play until the passive investors achieved a 13% IRR.

Unless there’s a refinance or sale of the asset, a secondary hurdle is rarely hit.

Waterfall Calculation Example #2

In order to help you grasp this concept, let’s take a look at one more example of a waterfall with a simple split and a 7% preferred return:

An apartment complex Dr. CF invested in with three other doctors has an annual cash flow of $100,000.

In this example, the four limited partners take 7% off the top. So $7,000 goes to them paid out on a quarterly basis ($1750/quarter).

This leaves $93,000 to be distributed with a 70/30 split between the Dr. CF and his 3 colleagues and the sponsor respectively.

In this case, the sponsor would take 30% and the passive investors 70% of the remaining $93,000.

Bottom Line

The limited partners in real estate syndication deals provide the majority of the capital to the projects. Waterfalls are a way to help protect that capital plus incentivize the sponsors to produce the highest returns possible.

Waterfalls can be structured in a number of ways and is up to you to understand how you’re potentially compensated before investing.

Join the Passive Investors Circle