5 Best Ways To Invest 50K Wisely For 2024 And Beyond

What’s the best way to invest 50K? This question was recently posted on a doctor-finance private Facebook group that I’m privy to.

I was amazed at the number of responses and broad range of answers regarding the best investment strategy.

Having an extra $50,000 is a great problem. It could come from an inheritance, tax refund, lottery win, sale of a property, life insurance proceeds, or other types of investments.

No matter the source, you want to make sure it’s invested wisely. (After reading this and you’re still not sure what to do with it, contact me and I’ll give you my mailing address:) )

Check Yo Self

Before deciding on any investment decisions, I suggest you check yo self before you wreck yo self.

I couldn’t pass up an opportunity to use that line, sorry. 🙂

Start by asking yourself, “Am I in a position to invest all or part of the money“?

There are two important financial areas to consider before moving forward:

- Emergency Fund

- Debt (high-interest)

Emergency Fund

An emergency fund helps to protect against the unexpected. You never know when the transmission is going to go out or the refrigerator decides to stop working.

Having an account set aside to handle these issues is one of the 5 short term financial goals I’ve discussed in the past.

Debt

If you have any consumer debt, excluding your house, throwing all of the money towards it should be done before investing it.

What’s the point in investing in mutual funds such as the Vanguard Total Stock Market Index and earning 7-8% a year when you have credit card debt with sky-high interest rates?

There are different schools of thought on this, but I agree with Dave Ramsey on this one. He recommends not investing until everything is paid off, minus the house. I see too many people making recommendations to invest and keep the lower interest rate loans around.

Most doctors graduate with a large amount of student loan debt. They tend to have other debt such as credit cards and vehicle loans too. The problem with not paying them off to invest gets more complicated with something called “lifestyle creep.”

Lifestyle Creep

According to Investopedia, lifestyle creep occurs when an individual’s standard of living improves as their discretionary income rises and former luxuries become new necessities.

It’s almost a given that the more someone makes, the more they spend. They tend to adhere to the rule, “have money, spend money“. Think about the last time you got a raise.

What did you do with it?

Unfortunately, in the U.S., a person is labeled a failure if they decide to move down in life.

For the person who gets a new iPhone for $600, that same person doesn’t think twice when upgrading to a newer version for $900.

If they’d gotten a lesser model, their friends and family members would’ve probably wanted to know if they were in a financial crisis.

The same goes for vehicles. I remember when a local doctor’s wife went from driving a Lexus to a Honda. I couldn’t help thinking that maybe they were having financial trouble. Unfortunately, society has taught me to react in this fashion.

Here’s a scenario that you may relate with:

Dr. Sparky is three years out of his Ear, Nose, and Throat residency, and things are on the up and up. He’s married, with two kids and one on the way. His income has steadily increased, and he plans to make partner in a three-doctor group within four years.

He has just over $300,000 remaining in student loans, $640,000 mortgage, $75,000 in vehicle loans, $1500/month in hunting club dues and recently joined a country club!

Last year, he received a $50,000 bonus and has to decide what to do with it.

He looks at the list of loans and realizes that he can easily make the minimum payments on all of them.

He’s a rich doctor, remember?

He realizes that he hasn’t been on a vacation with his wife in over a year, and she needs some R&R, especially while she’s expecting.

When he becomes a partner, his income will increase over 30%. So, instead of using the $50K to pay down debt, he decides to surprise his wife with a trip to Hawaii!

Three years ago, he attended a medical conference at the Four Seasons in Maui and can’t ever imagine staying in a “regular” hotel room again.

Do you see how this “lifestyle creep” can blur our vision?

On a personal note, I still remember attending a meeting at the Dallas Ritz Carlton about 13 years ago. At the time, I had never stepped foot in a high-end hotel/resort.

For those of you who have stayed at a Ritz Carlton, you know that their customer service is top-notch. I loved it so much that Mrs. Debt-Free calls me a hotel snob. Now, when traveling, I tend to gravitate towards the customer-service-oriented hotels first.

This is a perfect example of a former luxury that has become a new necessity.

Determine Your Risk Tolerance Level

How much risk can you take? Before deciding what to do with 50K, do yourself a favor and assess your risk tolerance level first.

By doing this, you can choose an investment strategy that matches your unique situation.

Everyone is different. What’s right for me may not be for you.

What is risk tolerance?

Your risk tolerance level is the amount of volatility and uncertainty you can withstand in your time horizon and investment portfolio.

In other words, how much money can you stomach to lose before crying “uncle“. This will tell you what type of investor you are.

Are you more comfortable with low-risk investments that yield lower returns, or do you shoot for higher returns with riskier asset classes?

The choice is yours, and that’s why it’s called personal finance.

There are a few factors to consider when assessing your own risk tolerance level:

Age

This is probably the most important factor to consider. The younger you are when you start investing, the better. Why? You’ve got more time on your side compared to a person who only has a few years left until reaching retirement age.

Younger investors can afford to make mistakes early on and still have enough time before retirement to make up for it. Older investors don’t.

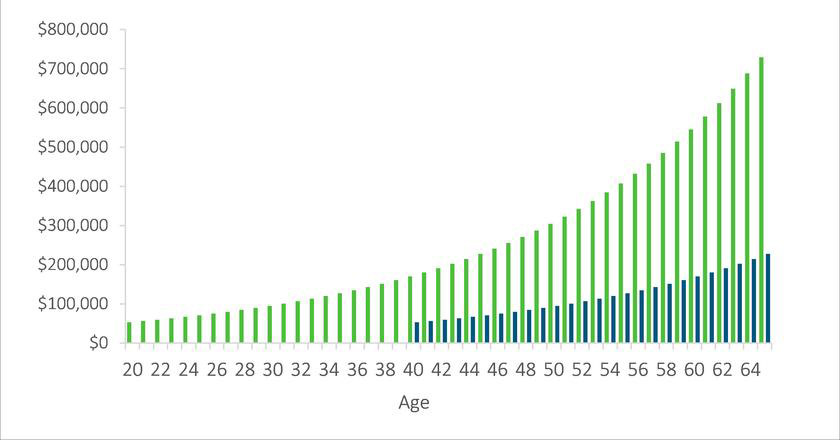

Here’s an example from FutureAdvisor.com that shows how a younger investor benefits from the power of compound interest.

The example below is for someone who wants to retire at 65, invests $50K, and expects a 6% annual return.

If they invested at age 20, they’d have over $729,000 in retirement savings without adding another cent to the account.

Take a look at the difference if they’d started 20 years later at age 40. At age 65, the total amount would only have grown to $230,000.

That’s a $499,000 difference. This is a great example showing that how long you invest can be more important than how much you invest.

The emergency fund

We discussed the emergency fund briefly earlier. One of the easiest ways to be able to handle financial emergencies is to build enough to cover three to six months worth of expenses.

Considering a riskier type of investment before doing so could lead to a financial crisis.

Your employment status

For those who have careers that afford them a steady income, a riskier investment strategy is possible.

On the other hand, those that are self-employed or work part-time, and their income is more variable, should consider a lower risk investment approach.

Top 5 Ways to Invest $50,000

Once you’ve funded an emergency account, paid off consumer debt and determined your investment risk tolerance level, it’s time to start investing.

While there are plenty of investment options to choose from, consider taking these steps in the order provided:

1) Employer-Sponsored 401(k) Plan

If your employer offers a 401(k) with a match, then this is a good place to start investing.

Use your $50K to max it out, which is $23,000 a year as of this writing.

If that seems too much to contribute to one account, then at least invest enough to take full advantage of your employer’s match.

The most common type is 50 cents per dollar up to a specified percentage of pay, commonly 6%.

For someone who makes $100,000 a year and the employer matches up to 6 percent of the salary at a 50 percent match, then contributing $6,000 a year will net $3,000 a year in employer match, which is essentially free money.

I encourage all of my employees to invest in the group plan offered at our practice. There’s one who always makes excuses as to why she doesn’t have the time to sign up.

My reply to her is the same each time I mention it: “I’m willing to give you free money, and you’re turning it down for no reason.”

2) Roth IRA

Another best option to invest $50K is with a Roth IRA. Once you’ve reached your annual limit on your 401(k) contribution, consider maxing out a Roth. The current annual contribution is $7,000.

A great advantage of this retirement account is that it allows you to access your money tax-free without penalty.

Since the contribution is made with after-tax dollars, you don’t need to worry about paying tax on future profits.

Also, the time you withdraw the money or why you need it doesn’t matter.

This is unlike taking money out of a 401(k) before the age 59.5.

You can read more about 401(k) withdrawal exceptions here.

3) 529 Plans

Another good way to invest $50K is in your children’s future with a 529 plan.

A 529 plan is a state-sponsored college investment plan. The major benefit of investing $50,000 in a 529 plan is that it allows your money to grow tax-free as your children grow up.

Here are some other 529 features you should know:

- In most states, there’s no age limit for distributions. For example, if your 30-year-old decides to go back to school, they are not penalized for using the money.

- There are no income restrictions to contribute.

- Contributions are subject to gift tax exemption limits, which are currently $15,000.

- You’re allowed to superfund 529 plans, which means you can make up to five years of contributions at once.

- Withdrawals are federal income tax-free and state income tax-free in most states.

- Withdrawals on non-qualified expenses are subject to taxes.

4) Index Funds

Once you have contributed the maximum annual amount to your 401(k), Roth IRA, and 529 plan, you may want to look into other investment funds for any leftover money.

One option is the index fund. An index fund is a mutual fund or exchange-traded fund (ETF) that is designed to track a specific index of:

- stocks

- bonds

- or other type of investments

This way, you get to take advantage of all the stocks that are a part of the index without having to buy individual stocks.

For example, an S&P 500 index fund would invest in all 500 components of that market index in order to replicate its performance.

Don’t take my word for it.

Here’s what Warren Buffett has to say about index funds (you can start at the 2-minute mark if 3:14 is too long for you).

Three advantages of index funds are:

- Passive management – Many funds are actively managed via a fund manager. Not index funds. This means that less of your investment goes toward fees and expenses.

- Low cost – By being passively managed, they tend to have a lower overall cost vs active investing.

- Tax-efficient. Index funds pay fewer dividends vs actively managed funds. They also have a low turnover rate. (Low turnover refers to the number of funds that have been replaced, or turned over, during a given year, which results in capital gains taxes.) Low turnover = lower taxes

5) Real Estate Investing

At this point in my career, my favorite investment vehicle is real estate. Sure, you can go out and purchase homes or apartments and become a landlord. But this isn’t the type of real estate I’m talking about.

The other type of real estate that you could invest in that doesn’t require you to fix clogged toilets is passive investing real estate.

I initially started off investing in crowdfunding sites but after I loss my shorts on a deal, I began REALLY learning the process and in time have found syndications to give us the best return for our money.

Syndications (My favorite)

Here’s a brief video over I put together of what’s involved in investing in real estate syndications.

A syndication is simply the pooling of funds from a group of investors in order to purchase a property that’s more expensive than any of them could have afforded on their own.

As a busy professional, you more than likely don’t have the time (like me), to be a landlord.

These alternative investments are hands-off, where you can still get the fantastic tax benefits and the mailbox money, aka cash flow or passive income!

Bottom Line: Deciding How To Invest $50K

How to invest $50k depends on your personal financial situation and goals. Remember, what’s right for me may not be right for you.

Here’s a brief summary of how to invest $50K:

- Set up an emergency fund to cover 3-6 months of expenses

- Pay off all high-interest debt (i.e. credit cards)

- Invest in an employer-sponsored 401(k) plan (at least be sure to invest enough to take full advantage of your employer’s match)

- Max out a Roth IRA

- Fund a 529 plan for your kiddos

- Index funds

- Real estate syndications

Never invest in anything you don’t understand. If you’re not a do-it-yourself investor and feel unsure about where your money will best serve you for your future goals, consider consulting a financial planner for guidance.

Join the Passive Investors CircleFAQs

What should I consider before investing $50k?

Before investing $50k, consider your investment goals, personal circumstances, and the level of risk you’re comfortable with. Consulting a financial advisor can help tailor an investment strategy to meet your long-term growth needs and retirement plans. It’s important to review past performance of financial products, understand market conditions, and consider the impact on your taxable income. Due diligence is key when evaluating different ways to invest your amount of money.

Is investing in real estate a good option for my $50k?

Real estate investments can be a great way to diversify your portfolio, especially with options like real estate investment trusts (REITs), rental properties, and real estate syndications.

However, it’s essential to consider the real estate market conditions, property value, and whether it’s a good time to invest. Real estate investors should be prepared for the responsibilities that come with property ownership and consider factors like down payments, higher interest rates, and rental income when evaluating if this is the best option.

How can exchange-traded funds (ETFs) benefit my investment strategy?

Exchange-traded funds (ETFs) and shares ISAs can be good options for individual investors looking to achieve long-term growth without investing much money directly into the stock exchange. ETFs offer diversification across various financial products and sectors, potentially reducing the risk associated with market fluctuations.

What are the benefits of high-yield savings accounts and certificates of deposit for my $50k?

High-yield savings accounts and certificates of deposit are considered safer investment options, providing a secure place to grow your money while still earning interest payments. These financial products are suitable for individuals with a lower risk tolerance or those looking to maintain a liquid emergency fund. While they offer lower returns compared to stocks or real estate, they can be a good idea for part of your investment strategy, especially in periods of higher interest rates.

How do I decide between investing in commercial vs. residential property with my $50k?

Deciding between commercial and residential property investments depends on your financial goals, risk tolerance, and level of involvement you wish to have. Commercial property often requires a larger down payment and comes with longer lease terms, which can lead to stable long-term rental income but may also be affected by economic downturns. Residential property can be more accessible for new investors and may offer more flexibility in terms of lease agreements. Perform due diligence, assess market conditions, and consider consulting a real estate or financial adviser to determine which type of property aligns best with your investment strategy.